It is now clear that Covid-19 is not just a short, sharp shock. The GDP of emerging markets and developing countries will plunge by -3.3% in 2020 – the only decline recorded in the post-war era. Extreme poverty is projected to rise by 150 million people, and the impacts on employment, education and health will be far deeper and more widespread than after the global financial crisis a decade ago.

Advanced economies are aggressively utilising counter-cyclical fiscal stimulus measures to alleviate the impact of the crisis, but most developing countries do not have that luxury. With donor aid budgets under pressure, the International Monetary Fund (IMF) facing its own constraints and private financial flows drying up, multilateral development banks (MDBs) have a major role to play in the global recovery.

This note provides:

- a brief reminder of the continued case for investing in MDBs;

- a review of the lending response to date and prospects for the coming year by the World Bank and four major MDBs; [i]

- and options to increase the scale of financing to support recovery.

The focus of this note is on the supply of financing to the public sector. It does not address several other important issues related to MDB crisis response, including debt sustainability, policy dialogue, private sector support and efforts to streamline MDB processes, among others.

The case for investment in MDBs

Decisions on how to allocate aid budgets directly or via multilateral organisations are complex. Bilateral aid programmes are principally meant to help achieve foreign policy objectives, offer greater visibility (PDF) of development interventions and more control over how development budgets are spent. Aid nationalism is also becoming stronger in governments’ responses to the Covid-19 crisis.

Despite pressing budget constraints for bilateral donors, the evidence for investing in the multilateral development banking system is compelling – even more so during this unprecedented crisis.

First, MDBs offer very good value for money.

For example, the World Bank’s International Bank for Reconstruction and Development (IBRD) window had lent over $700 billion and generated $55 billion in net income by 2018, based on shareholder capital of only $16.5 billion – 46 times leverage, compared to between 0.3 and 22 times for blended finance. The total paid-in capital to IBRD since 1944 represents about 10% of aid disbursements in just one year by members of the Organisation for Economic Co-operation and Development's Development Assistance Committee (OECD DAC).

Second, MDBs provide countercyclical lending at more affordable rates for most borrowing countries than what markets can offer.

Many governments cannot borrow domestically or internationally, and central banks might not have enough firepower. MDBs can provide the type of risky long-term investments needed to support structural changes in economies in a way that commercial banks or capital markets might avoid.

Third, soft windows of MDBs channel more resources to the poorest countries and those most in need than the DAC average.

The concessional lending windows of the African Development Bank and World Bank allocate 64% and 36% of their resources to the most severely fiscally-constrained countries respectively, far more than the 25% average of DAC bilateral donors.

Fourth, MDBs are generally more effective than bilateral donors.

Multilateral development organisations score better than bilateral donors in the development effectiveness agenda, especially in terms of alignment to national priorities and policy engagement. Recipient country governments prefer working with multilateral organisations than bilateral donors. Multilateral actors are also perceived as more trustworthy, flexible and responsive and with valuable technical skills and policy expertise.

Finally, as countries move up the income per capita ladder and bilateral donors phase out their programmes, MDBs stay offering policy advice, technical support and financing.

These will be critical to fight the consequences of the Covid-19 pandemic. For middle-income countries (MICs) badly hit by the crisis, like India, South Africa and much of Latin America, MDBs are critical partners, especially as private investors pull back.

The scale of MDB support during the crisis to date

The World Bank and four major regional MDBs have responded quickly to Covid-19. However, financing falls well short of their response to the global financial crisis, despite the much more severe and widespread nature of the current crisis.

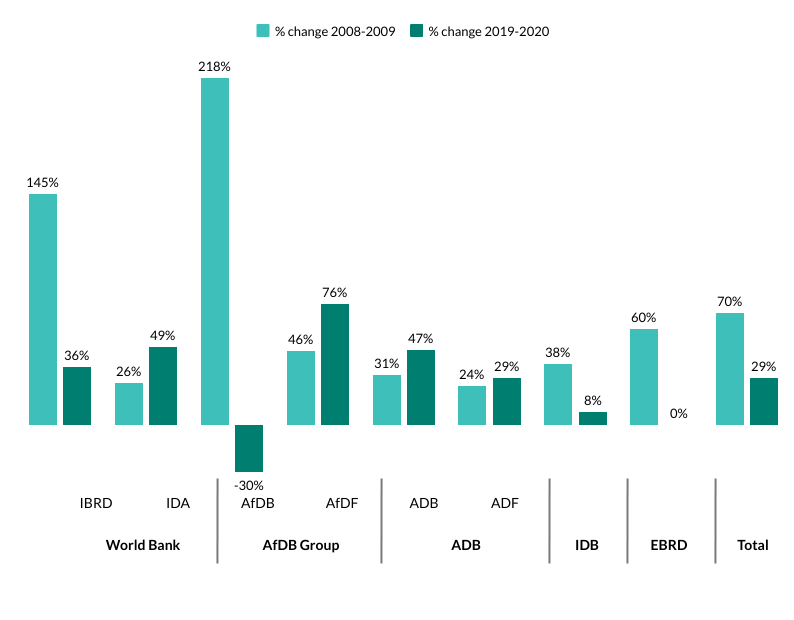

MDBs have expanded lending by about 30% relative to 2019, compared to 70% after the global financial crisis (see graph one), and lending will revert to previous levels next year. The principal reason for this limited response is insufficient financial capacity compared to a decade ago.

Graph one: MDB lending increase in Covid-19 is less than half that of global financial crisis

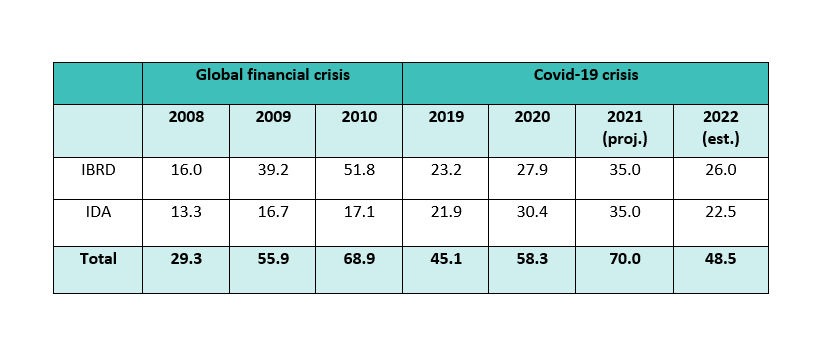

Table one: World Bank lending – global financial crisis versus Covid-19 (real $ billions, fiscal year)

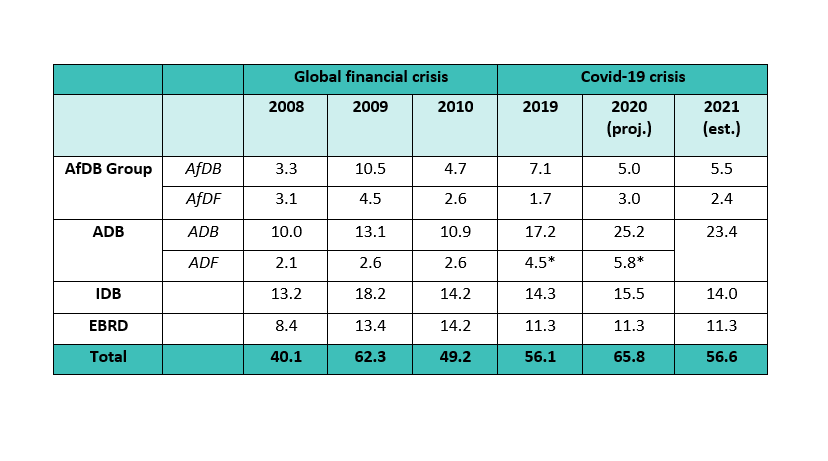

Table two: regional MDB lending – global financial crisis versus Covid-19 (real $ billions, calendar year)

1. World Bank: strong support for low-income countries but less for middle-income borrowers

Lending by the International Bank for Reconstruction and Development (IBRD) for middle-income borrowers rose to $27.9 billion in FY2020, up 20% over the previous year and evidence of a fast if limited response to the crisis this spring. Lending is projected to rise to $35 billion in FY2021, and then decline to $26 billion in FY2022. This response is well below IBRD’s nearly tripling of lending in 2009 after the global financial crisis, and even higher lending in 2010.

The main reason for IBRD’s underwhelming response to Covid-19 is a lack of financial capacity. This may seem surprising in light of IBRD’s 2018 capital increase, but that amounts to only about $7.5 billion of actual cash capital, paid in over the next five years. While certainly helpful, it does not permit a substantial increase in lending in the current emergency. IBRD’s Sustainable Annual Lending Level for FY2021 (PDF) was $25 billion. On top of that, IBRD will make use of an additional $10 billion emergency buffer to reach $35 billion in lending for the year.

Even within these constraints, however, progress toward implementing the FY2021 lending programme in the first quarter (PDF) from June to September is lagging. IBRD disbursements have stayed high at $7.4 billion compared to around $3 billion a year ago, but new loan commitments actually fell substantially in the past quarter to $3.1 billion, only 9% of the FY2021 annual lending target. IBRD’s benchmark equity-to-loans ratio now stands at 22.6%, essentially unchanged for the past five quarters, suggesting that it has not yet made significant use of even the limited lending space it does have available to address the crisis.

The International Development Association (IDA) window for low-income borrowers quickly ramped up lending between April-June 2020, with commitments in FY2020 (PDF) jumping about 40% over FY2019 and a further rise to $35 billion projected for FY2021. This is well above the 25% increase during the global financial crisis. Disbursements also rose in the last quarter of FY2020 (April-June) by $3.7 billion (20%) compared to the same period in 2019.

By front-loading 43% of its FY2021-23 resource envelope in FY2021, IDA will be forced to reduce lending to a projected $22-23 billion each year in FY2022 and FY2023 in lieu of further donor resources. Due to recent reforms (PDF) to the IDA’s financial model, it is possible to issue bonds to raise more resources, but it would have to offer additional loans at slightly above normal IDA financial terms. This would bump up against debt sustainability concerns and IMF limits on non-concessional borrowing.

2. African Development Bank Group: headroom restrictions limit response

In April, the African Development Bank Group (AfDB) announced that it would target $10 billion in lending this year in response to Covid-19. The lending package calls for $7 billion from the non-concessional AfDB window, about the same as in 2019 and far below the nearly tripling of lending a decade ago. But AfDB will likely approve only about $5 billion this year due to insufficient financial capacity, falling well short of its target. AfDB has scaled up its use of budget support lending to over 30% of approvals thus far in 2020, double the normal 15% ceiling.

AfDB’s 2019 capital increase did little more than rescue the bank from a dire financial situation and did not meaningfully boost lending capacity. Only 6% of the $115 billion increase was actually cash capital, and it is paid in over roughly 10 years. By March 2020, AfDB had already almost used up its lending headroom. AfDB is now in breach of its internal capital adequacy limits, and lending in 2021 is projected to be about $5.5 billion.

The African Development Fund concessional window is better positioned to reach its $3 billion lending target for 2020, 50% above the figure in 2019 and similar to its response to the global financial crisis. As with IDA, the African Development Fund is funded mainly by donor contributions and net income allocations from the AfDB window. Its latest replenishment of $7.7 billion covers 2020-2022, giving the bank sufficient resources on hand. The African Development Fund has substantially scaled up fast-disbursing budget support operations, although precise estimates are unavailable.

These commendable efforts to front-load resources will pose problems going forward. The African Development Fund is committing 39% of resources in 2020, leaving roughly $2.4 billion per year for 2021 and 2022 – a substantial drop in support for its 37 borrower countries. Deteriorating public debt profiles due to the crisis will likely mean a higher level of grants in 2021 and 2022, which would consume resources even more quickly. Unlike IDA, the African Development Fund cannot issue bonds to raise additional resources.

3. Asian Development Bank: quick and strong support, but more is possible

The Asian Development Bank (ADB) has quickly ramped up lending in response to the Covid-19 crisis. It announced a $20 billion support package on 13 April 2020, of which about $13 billion is fresh resources. ADB expects to commit $31 billion in 2020 ($25.2 billion non-concessional and $5.8 billion concessional), a 43% jump over 2019. By June 2020, non-concessional disbursements had already jumped by $5 billion over the same period in the previous year as a result of fast-disbursing budget support loans. Lending is projected to come back down to $23.4 billion in 2021.

ADB’s greater ramp-up capacity is directly due to the restructuring of the Asian Development Fund (ADF) concessional window in 2017, which acted as a massive $34 billion paid-in capital increase. As of 30 June 2020, ADB was using only two-thirds of its lending headroom, giving it substantial flexibility to increase lending further. Grant funding for 10 lower income nations is more restricted due to four yearly replenishment rounds, with total grant resources expected to remain flat for 2021-2024.

4. The Inter-American Development Bank: fast but limited response, despite severe crisis impact

Latin America’s economy has been badly hit by Covid-19, with regional GDP set to fall by a devastating -8% in 2020. The Inter-American Development Bank (IDB) has reacted quickly to accelerate project approvals and disbursements, but overall lending is projected to tick up by only about $2 billion this year to $15.5 billion (15% above 2019) before dropping back to around $14 billion in 2021. This compares to a 40% jump in lending after the global financial crisis. As of the end of September, the IDB had approved $11.3 billion in new loans, and net disbursements were $2.5 billion higher than in the same period in 2019.

As with IBRD and AfDB, insufficient financial capacity is the main reason behind IDB’s limited response. Standard and Poor’s measure of IDB capital adequacy strength is a notch below that of IBRD, ADB and EBRD. The bank’s capital situation has been further complicated due to downgrades and negative outlooks for several sovereign borrowers as well as Venezuela’s loan repayment stoppage to IDB. Both the outgoing and incoming presidents of IDB have called for more shareholder capital to bolster lending capacity.

5. The European Bank for Reconstruction and Development: capacity available but shareholder mandates restrict crisis response

The European Bank for Reconstruction and Development (EBRD) has no plans to increase the overall lending envelope for 2020. Lending is expected to be about $11 billion this year, similar to 2019. The bank is focusing on quickly providing liquidity to private sector clients and state-owned enterprises to help them through the crisis. No emergency support to member governments is planned, despite major downturns in some eastern European countries. EBRD had approved $10 billion by the end of October, up 30% from 2019.

EBRD has no authorisation from shareholders to deviate from the bank’s statutory mandate to promote private sector development and economic transition, which limits scope for crisis lending to member governments. Financial capacity is not an immediate restriction. The bank’s 2019 financial statement shows that it has about one-third of its capital adequacy headroom still available and ratings agency calculations also indicate substantial room to expand.

How to increase the scale of MDB investment in recovery

Overall, the response of the World Bank and these four regional MDBs is not commensurate with the scale of the Covid-19 crisis. It is well short of how the MDBs reacted after the milder and less widespread global financial crisis. The limited MDB response is, above all, due to restricted lending headroom compared to a decade ago.

The G20 and the shareholders of the major MDBs should consider a series of short- and medium-term policy options to boost the financial capacity of the MDBs in response to the Covid-19 crisis.

Urgent support is needed for both low-income countries (LICs) as well as MICs that have been badly affected by the crisis and are critical to help drive the global recovery.While some of the options below come with a degree of risk, they pale in comparison to the economic and social risks if MDBs do not dramatically step up their efforts in response to the worst global crisis in decades.

The next six months: short-term policy options

Donors should commit a share of their annual aid budgets to provide additional resources to the concessional lending windows of the World Bank and AfDB.

IDA and the African Development Fund will have to dial back lending in the next two years without more help. LICs were already facing a financing gap in the order of $50 billion per year to achieve the Sustainable Development Goals, and the damage wrought by the Covid-19 crisis has increased that gap by 70%. Absent any additional resources to these windows, flows to the poorest countries will fall just as investments in recovery are most needed.

Discussions should start immediately and be finalised by the spring, to provide clarity for MDBs and recipient nations. Donors can either provide supplemental funding to the existing concessional envelopes (the option advocated by the World Bank) or advance the upcoming scheduled replenishments by one year. Either approach would allow IDA and the African Development Fund to continue high levels of crisis lending into next year.

IDA should be authorised to issue more bonds to raise resources to on-lend at non-concessional terms to specific countries with sufficient demand and debt space. This should be in conjunction with temporary waivers from the IMF on non-concessional borrowing limits on a case-by-case basis. Donors can contribute a small amount of resources to bring financial terms down to concessional level.

Increase and accelerate resources to middle-income borrowers

Many of the world’s major MICs have been severely hit by the Covid-19 crisis, while financial flows have dried up. Some relatively low-cost measures could have significant short-term gains.

Shareholders can authorise IBRD and IDB to temporarily relax internal capital adequacy rules to allow for more lending, while maintaining a AAA rating. Based on Standard & Poor’s methodology, this could open up at least $120 billion and $30 billion in headroom at IBRD and IDB, respectively.[ii] New lending could be done at shorter maturities and higher interest rates (as IBRD is already doing for some loans), and capital adequacy limits could revert as the crisis eases. Shareholders should push IBRD to accelerate its use of the lending space it does have available, particularly through a more streamlined use of fast-disbursing budget support loans.

Paying already-committed new capital to AfDB ahead of schedule would help address lending constraints. The schedule agreed in 2019 is stretched over 10 years, and shortening that pay-in period for non-borrower shareholders would give AfDB additional lending headroom. Obtaining temporary callable capital from a AAA-rated shareholder would also ease current pressure from Fitch’s bond rating methodology.[iii]

ADB and EBRD should make greater use of available lending headroom. Several member countries of both these MDBs would benefit from greater financial support to face the ongoing health emergency, social protection and rebuilding efforts. Keeping lending space on reserve makes little sense in the face of a crisis of this magnitude.

2021-2022: medium-term policy options

The capital constraints facing the MDB non-concessional windows must be addressed. To do so, shareholders have four main options, which are not mutually exclusive.

Provide more shareholder capital to the non-concessional windows of the World Bank and IDB

A capital increase is the first-best option to position the MDBs to support the global recovery and build back better. Additional share capital would represent a very small share of annual donor aid budgets, and will leverage MDB lending for years to come. The political and fiscal challenges are real, but well worth overcoming to put the MDBs on a strong financial footing.

Re-evaluate MDB capital adequacy limits to increase lending headroom with existing capital, in coordination across MDBs and with G20 support

Easing capital adequacy constraints within the bounds of a AAA rating can free up substantial lending headroom. One option is to create a “two-tier” capital adequacy approach that temporarily eases limits in times of crisis, reducing the need for MDBs to sit on emergency capital buffers. This should be done as part of a broader review of MDB capital adequacy by an external agency, as recommended by the G20’s Eminent Persons Group (PDF) and others (PDF).

Target a sub-AAA bond rating for AfDB

If keeping a AAA rating means AfDB must cut back on lending during the worst crisis in decades, it is time to change the policy. Targeting a AA rating would still result in very inexpensive funding and would allow AfDB to dramatically expand its lending. Options like obtaining hybrid capital, which AfDB management has floated, are unlikely to be viable. A sub-AAA rating does not make sense for the other MDBs, particularly if shareholders embrace the proposals above.

Further explore balance sheet optimisation

Balance sheet optimisation should also be further explored, although gains will likely be marginal and come with trade-offs. Four options are:

- Co-financing platforms for public sector lending, conceptually similar to the International Finance Corporation’s (IFC) Managed Co-Lending Portfolio Programme, could seek funding from official sources like sovereign wealth funds or central banks. These resources would be unleveraged and thus not as powerful as share capital, but still provide additional firepower.

- Portfolio guarantees from highly-rated shareholder governments, like those done in recent years by the ADB and the World Bank, can increase MDB lending capacity.

- AfDB, IDB and IBRD first utilised portfolio exchanges to ease capital adequacy constraints in 2015. ADB just approved a policy permitting such operations, and bringing in MDBs like the European Investment Bank would help make more transactions viable.

- Risk transfers to the private sector via securitisations or credit insurance for loan portfolios have been used minimally by MDBs – notably by AfDB in 2018 – and have further potential, though mainly for private sector loans.

We thank Jessica Pudussery for excellent research assistance, Mark Miller for his guidance and feedback throughout and colleagues in MDBs for reviewing an earlier draft of the paper.

Footnotes

[i] Of particular note are the Asian Infrastructure Investment Bank (AIIB) and New Development Bank (NDB), both of which have ample lending headroom. AIIB is targeting $13 billion in additional lending by October 2021, while NDB is aiming for $10 billion above its originally planned lending. The Islamic Development Bank has announced an additional $2.3 billion in lending in response to the crisis. CAF, the Central American Bank for Economic Integration and Trade and Development Bank in Africa have announced extra financing as well, although they face capacity constraints.

[ii] The target 16.6% Risk Adjusted Capital ratio from S&P targeted to achieve this headroom is conservatively within the range needed for IBRD and IDB to achieve a AAA rating under S&P’s methodology. Numbers in this paper are based on more recent data than used by Humphrey, but the methodology is the same. Fitch and Moody’s have different methodologies, but like S&P account for callable capital in a way that the MDBs themselves do not, which creates substantial lending headroom.

[iii] This is driven in part by Fitch’s downgrade of Canada to AA+ and negative outlook on the U.S., which impact the amount of AfDB callable capital from AAA shareholders.

Graphs and tables

World Bank and EBRD are loan commitments, while AfDB and IDB are loan approvals. ADB reports approvals in 2008-09, but commitments in 2019-20. Does not account for exchange rate movements affecting EBRD and AfDB. All World Bank data is for fiscal year (July-June); others are calendar year. To capture World Bank early response in the spring of 2020 and avoid a distorting comparison, the average of FY2020 actual and FY2021 projected lending are compared to FY2019 for IBRD and IDA.

Adjust for inflation with 2019 as base year. Reports loan commitments. World Bank’s fiscal year runs July-June. It began responding to the crisis at the end of FY2020, making these numbers not directly comparable to the other MDBs.

Adjust for inflation using 2019 as base year. Does not account for exchange rate movements affecting EBRD and AfDB. EBRD are loan commitments, while AfDB and IDB are loan approvals. ADB are approvals in 2008-10, but commitments in 2019-20. AfDB numbers for 2020 reflect projected lending, not the target announced in April of $7 billion. For 2019-2021, “ADF” denotes grants from ADF window and concessional lending from ADB window, to make it comparable to 2008-2010.